Serbia’s Okun mirage: When growth and jobs refuse to march in step – Part III

The evidence is not nihilistic, but it is conditional, and policy has to live with that.

1. What Serbia’s evidence says about Okun, and what it refuses to say

Put the three instalments together and the Serbia story becomes clearer, and less comforting. The charts in Part I show an economy where output and unemployment do often move in opposite directions, especially in crisis years, but where timing is lumpy and the relationship looks episodic rather than mechanical. Part II then does the hard work of asking whether this intuition survives formal scrutiny. The answer, as the study presents it, is: “sometimes in spirit, rarely in a way you can bet the policy house on.”

That is not a failure of Okun’s intuition. It is a warning against treating an empirical regularity as a universal law, particularly in a country whose macroeconomic history includes large discontinuities and whose annual sample is short enough that statistical confidence can be expensive. The study itself foregrounds the small-sample problem (around 29 annual observations in the main window) and the plausibility that structural breaks suppress clean inference even when a break dummy is included.

The most important synthesis point is therefore not “Okun holds” or “Okun breaks.” It is this: Serbia’s GDP–unemployment linkage is visible in the narrative moments (crises and rebounds), but it is not robust enough, on the study’s tests, to support a stable long-run equilibrium story or a reliable predictive-causality story.

2. Where the relationship holds, and where it breaks

The study uses two ways of looking at Okun’s Law: a first-difference view (growth vs unemployment changes) and a gap view (output gap vs unemployment gap). The charts support the basic sign expectation in both, especially around major downturns, but the simple scatter/regression fit is weak in Serbia, negative slopes that do not become statistically persuasive and clouds of points that refuse to line up obediently.

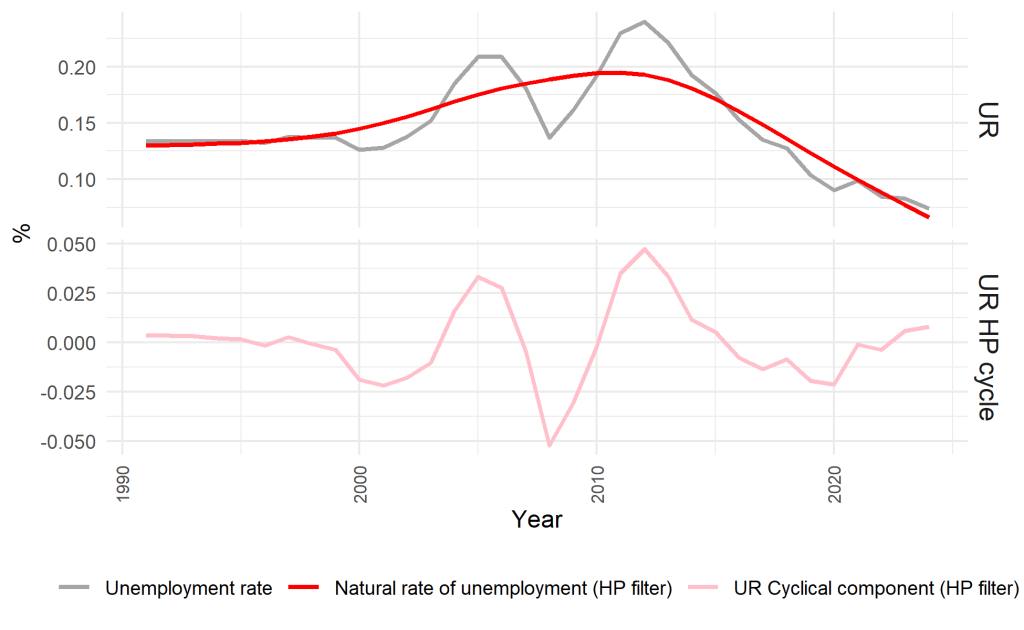

The gap series themselves are instructive even when the regression line is not. The study’s HP-filter gaps highlight negative output-gap periods around 2000–2002, 2009–2011, and 2020–2021, with corresponding episodes of positive unemployment gaps, exactly the cyclical slack story Okun fans want to tell. But the study also stresses inertia and asymmetry in a descriptive sense: unemployment slack tends to dissipate more slowly than output recovers, and Serbia “rarely experiences large negative unemployment gaps” even in good times, suggesting that structural frictions may keep slack from fully vanishing.

Then comes the stern part of the story. When the study turns to formal testing and tries to establish a stable long-run anchor, the evidence becomes fragile. Unit-root diagnostics (DF-GLS and KPSS) support treating the levels variables (LGDP, UR) as nonstationary and the gap variables as stationary, with the unemployment gap showing particularly strong stationarity evidence. That pushes the modelling toward (i) differenced relationships for levels variables, and (ii) cyclical relationships among stationary gap variables.

But cointegration, what would justify a strong “long-run Okun equilibrium” story, does not receive robust support. Engle–Granger finds no cointegration; Gregory–Hansen offers only weak or near-significant hints under some break specifications; Johansen appears more optimistic in some configurations; and Bayer–Hanck, the combined (and conservative) check, refuses to reject “no cointegration” across the model variants it tests.

That sequence matters. It tells you how the study wants you to interpret Serbia’s Okun relationship: not as a timeless law with a fixed long-run coefficient, but as a relationship whose strength is disrupted by breaks and whose long-run stability is not empirically secured in this sample.

Finally, causality, the political economy temptation. The study applies the Toda–Yamamoto approach and finds no evidence of Granger causality in either direction for both gap and first-difference models, even with the 1999 dummy included. The synthesis then links this null result to the cointegration conclusion: if there is no stable long-run anchor and no short-run predictive precedence, then “causal” stories should be told with caution, and models that assume a cointegrating equilibrium or a strong directional mechanism are “not empirically justified” here.

3. The policy meaning: Growth, slack, and labour-market adjustment

So what does a policy reader do with a relationship that exists in the graphs but evaporates under strict testing?

First, stop demanding a single coefficient to do a job it was never hired to do. The study’s evidence is consistent with a common-sense proposition: big output shocks matter for unemployment, but the mapping is not stable enough in Serbia’s annual data to be reduced to a neat rule-of-thumb. In practice, that means policy should focus less on “the Okun coefficient” and more on the mechanisms that make the coefficient unstable: adjustment lags, structural breaks, and persistent slack that does not fully disappear even when output improves.

Second, treat slack measures asymmetrically. One of the study’s more practical conclusions is about which gap you trust more. It argues that unemployment gaps can be used as cyclical indicators more confidently than output gaps in Serbia, while output gaps are more vulnerable to distortions from structural change and crises; policymakers should therefore lean more on labour-market slack indicators and treat output-gap estimates with greater caution around disruptive episodes.

Third, accept that “growth-first” narratives are incomplete if the data do not show reliable predictive precedence from GDP to unemployment in the causality tests. The study’s point is not that GDP doesn’t matter. It is that, in the tested annual framework, GDP does not systematically forecast unemployment changes, and unemployment does not systematically forecast GDP either, suggesting that the relationship may be mediated by other factors (including structural features of the labour market) rather than captured cleanly by a simple two-variable dynamic story.

With those caveats, we can still extract clear “usable truths” from the study, carefully framed.

Key empirical takeaways from Serbia:

- Output and unemployment often move in the expected opposite directions during major downturns and recoveries, but the relationship is weak and noisy in simple regressions for both first-difference and gap formulations.

- Level variables behave like drifting series (nonstationary), while HP-filter gaps behave like cyclical, mean-reverting series (stationary), especially the unemployment gap.

- Robust long-run cointegration is not supported once conservative combined testing is applied, and predictive causality is not detected in either direction under Toda–Yamamoto in this sample.

If those sound modest, good. In applied macro, modest claims are often the only honest ones.

4. EU-candidate context: Alignment pressure without overclaiming

Serbia’s EU-candidate status does not prove anything about Okun’s Law. But it does shape the policy constraints under which any Okun-style stabilisation strategy would operate.

EU alignment typically pushes candidate countries toward more predictable rule-making, stronger statistical harmonisation, and institutional convergence in labour-market policy practice. In a setting where the study’s results hint at structural frictions and breaks that complicate the growth–jobs mapping, that alignment pressure matters because it tends to emphasise policy credibility, labour-market institutions that are enforceable and transparent, and macro frameworks that reduce the frequency of “regime-like” disruptions. None of this guarantees a stable Okun coefficient. But it can reduce the likelihood that the labour market is repeatedly asked to adjust in chaotic, discontinuous ways, precisely the kinds of conditions the study treats as hostile to clean inference and stable relationships.

5. Practical takeaways

Serbia’s evidence in this study pushes toward policy realism: use Okun as a diagnostic lens, not as a mechanical policy calculator.

What this implies for policy design, in the study’s spirit:

- Labour-market policy: prioritize the institutions and practices that speed adjustment and reduce persistence of slack, since the unemployment gap shows inertia and rarely turns strongly “tight” even in better periods.

- Macroeconomic stabilisation: treat crisis periods as the times when the output–unemployment link is most operationally relevant, because the co-movement is clearest around large shocks.

- Measurement discipline: use unemployment-gap indicators confidently as cyclical signals, but treat output-gap measures with caution around breaks and disruptions, as the study explicitly advises.

6. What to watch next as the relationship evolves

The study’s pipeline is also a guide for what to monitor going forward. If Serbia’s Okun relationship is unstable because the economy is repeatedly pushed through breaks, then stability itself becomes a variable worth pursuing. If, alternatively, instability reflects structural labour-market features, then reforms that change matching, participation, and wage-setting would matter more than another decimal point of GDP growth.

Signals worth watching, consistent with the study’s framing:

- Whether gap measures continue to behave as stationary cyclical objects, especially the unemployment gap that appears most “well-behaved” in the unit-root diagnostics.

- Whether future data, with longer samples, begin to support cointegration more robustly, or whether conservative combined tests continue to reject a stable long-run anchor.

- Whether predictive precedence emerges in causality testing as the sample grows, or whether the relationship remains mediated by breaks and structural factors in ways that simple two-variable models cannot capture.

If that sounds like a cautious ending, it is. Serbia’s Okun curve is not absent. It is simply loose, like the title says, because the labour market is not a frictionless mirror of output. The policy task, then, is not to worship the coefficient. It is to make the economy a place where the coefficient has a chance to mean something stable.

References

Bayer, C., & Hanck, C. (2013). Combining non-cointegration tests. Journal of Time Series Analysis, 34(1), 83–95. DOI: https://doi.org/10.1111/j.1467-9892.2012.00814.x

Clemente, J., Montañés, A., & Reyes, M. (1998). Testing for a unit root in variables with a double change in the mean. Economics Letters, 59(2), 175–182. DOI: https://doi.org/10.1016/S0165-1765(98)00052-4

Elliott, G., Rothenberg, T. J., & Stock, J. H. (1996). Efficient tests for an autoregressive unit root. Econometrics, 64(4), 813-836. DOI: https://doi.org/10.2307/2171846

Engle, R. F., & Granger, C. W. J. (1987). Co-integration and error correction: Representation, estimation, and testing. Econometrica, 55(2), 251–276. DOI: https://doi.org/10.2307/1913236

Gregory, A. W., & Hansen, B. E. (1996). Residual-based tests for cointegration in models with regime shifts. Journal of Econometrics, 70(1), 99–126. DOI: https://doi.org/10.1016/0304-4076(69)41685-7

Hodrick, R. J., & Prescott, E. C. (1997). Postwar U.S. business cycles: An empirical investigation. Journal of Money, Credit, and Banking, 29(1), 1–16. DOI: https://doi.org/10.2307/2953682

Johansen, S. (1991). Estimation and hypothesis testing of cointegration vectors in Gaussian vector autoregressive models. Econometrica, 59(6), 1551–1580. DOI: https://doi.org/10.2307/2938278

Kapetanios, G., Shin, Y., & Snell, A. (2003). Testing for a unit root in the nonlinear STAR framework. Journal of Econometrics, 112(2), 359–379. DOI: https://doi.org/10.1016/S0304-4076(02)00202-6

Kwiatkowski, D., Phillips, P. C. B., Schmidt, P., & Shin, Y. (1992). Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root? Journal of Econometrics, 54(1-3), 159-178. DOI: https://doi.org/10.1016/0304-4076(92)90104-Y

Lee, J., & Strazicich, M. C. (2003). Maximum Lagrange multiplier unit root test with two structural breaks. The Review of Economics and Statistics, 85(4), 1082-1089. DOI: https://doi.org/10.1162/003465303772815961

Toda, H. Y., & Yamamoto, T. (1995). Statistical inference in vector autoregressions with possibly integrated processes. Journal of Econometrics, 66(1-2), 225-250. DOI: https://doi.org/10.1016/0304-4076(94)01616-8

Zivot, E., & Andrews, D. W. K. (1992). Further evidence on the great crash, the oil-price shock, and the unit-root hypothesis. Journal of Business & Economic Statistics, 10(3), 251–270. DOI: https://doi.org/10.1080/07350015.1992.10509904