Serbia’s GDP in the Long Cycle: Trends, Forecasts and Regional Synchronisation, 1995–2026

Part 1. Serbia’s GDP as a Quarterly Time Series

1.1 Introduction

Gross domestic product is the broadest single indicator of macroeconomic activity. It measures the value of goods and services produced in an economy and therefore provides a compact summary of expansions, recessions, recoveries and longer-term changes in productive capacity. In this analysis, Serbia’s GDP is observed quarterly from 1995Q1 to 2026Q1 and expressed as an index with 2021=100. The source is Eurostat’s quarterly national accounts dataset, namq_10_gdp. Two versions of the series are considered: the original series and the seasonally adjusted series obtained using X13-ARIMA.

The long period covered by the series is analytically useful because it contains several very different macroeconomic regimes. The late 1990s capture an exceptional period of disruption. The early and mid-2000s show post-crisis recovery and transition-era expansion. The late 2000s and early 2010s include the global financial crisis and its aftermath. The later part of the sample captures a more mature growth phase, the COVID-19 shock, the rapid post-pandemic rebound and the most recent moderation. This makes the Serbian GDP series a useful case for demonstrating how time-series tools can help separate long-run trend, seasonal variation, cyclical movement and exceptional shocks.

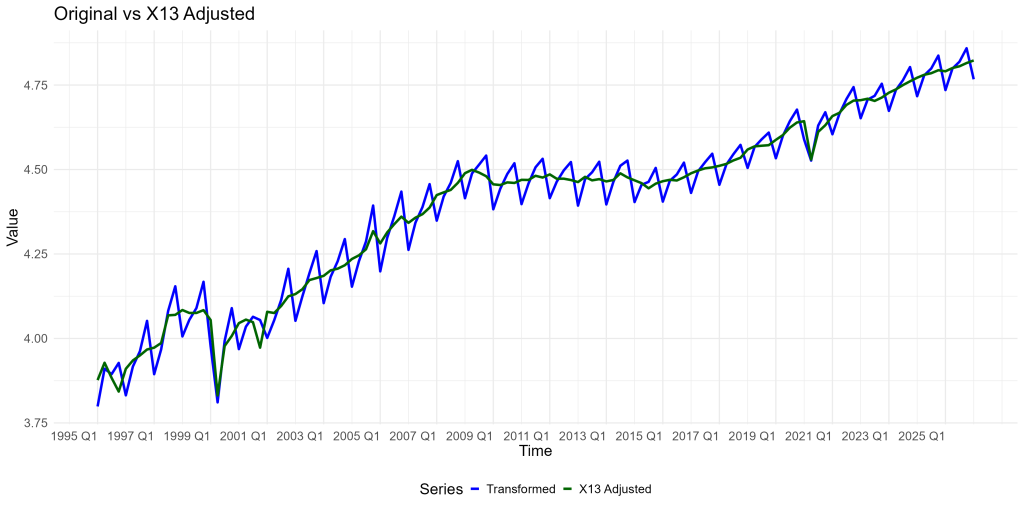

Figure 1 shows a clear long-run increase in Serbia’s GDP, but the path is far from smooth. The most dramatic visible decline occurs around 1999. After that, the series recovers and enters a period of relatively strong expansion in the 2000s. The global financial crisis is visible as a break in this expansion, followed by a slower and less uniform recovery. From the mid-2010s onward, the underlying direction is again upward. The COVID-19 shock in 2020 is clearly visible as a sharp but short-lived interruption, after which GDP rebounds relatively quickly. By the end of the sample, GDP is close to its highest observed level, although the most recent quarters look more like a mature expansion than a new acceleration.

The comparison between the original and seasonally adjusted series is important. Quarterly GDP contains regular within-year movements that are not, by themselves, evidence of changes in the business cycle. Seasonal adjustment removes these repeated calendar patterns and makes the underlying movement easier to interpret. In Figure 1, the adjusted series therefore gives a cleaner view of the trend and the cyclical turning points, while the original series reminds the reader that the raw quarterly data still contain regular seasonal variation.

1.2 Autocorrelation and persistence

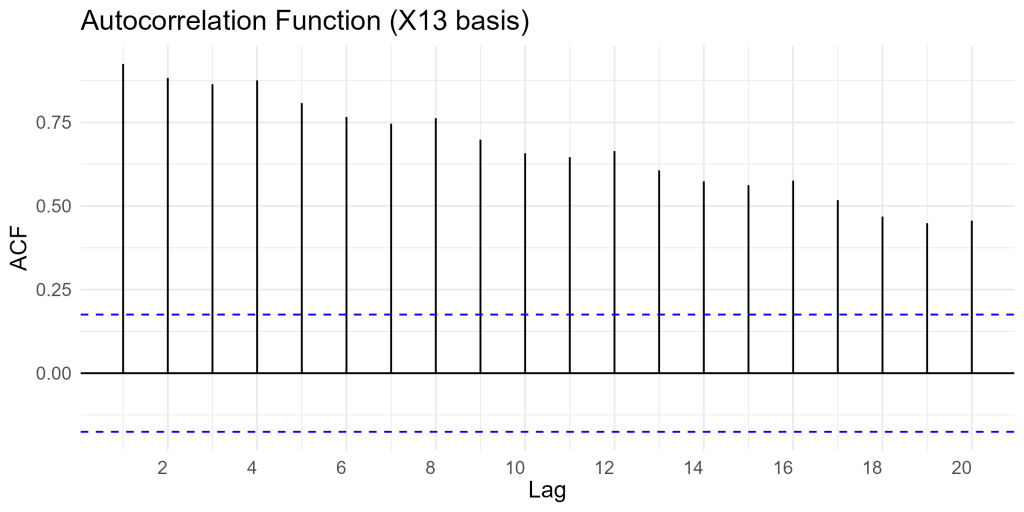

Figures 2 and 3, together with Table 1, show that Serbia’s GDP behaves like a typical macroeconomic level series: it is highly persistent. The autocorrelation function of the log-level series remains strongly positive over many lags. The first autocorrelation is about 0.925, which means that the level of GDP in one quarter is very closely related to the level in the previous quarter. This is not surprising. GDP does not jump randomly from one quarter to the next. It is shaped by accumulated capital, employment, productivity, institutional conditions, external demand and policy settings, all of which evolve gradually.

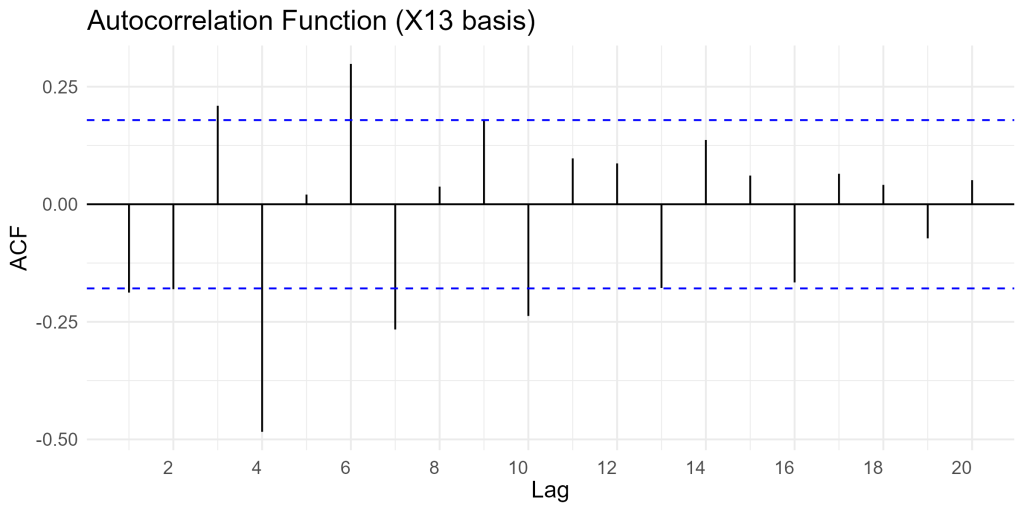

The picture changes when the log series is first differenced and seasonally differenced. Figure 3 shows much weaker autocorrelation after differencing, with several negative autocorrelations. This is exactly what differencing is intended to do. It removes much of the trend and seasonal persistence and shifts attention from the level of GDP to shorter-run changes. In practical terms, the original log-level series is appropriate for describing the long-run macroeconomic path, while the differenced series is more relevant for modelling quarterly growth dynamics and for ARIMA forecasting.

Table 1 gives a numerical summary of these features. The trend strength is extremely high, around 0.995, confirming that the dominant component of the series is long-run growth rather than stationary fluctuation around a fixed mean. Seasonal strength is also high, around 0.875, which justifies the use of seasonal adjustment. The KPSS statistic points to non-stationarity, while the reported number of ordinary differences and seasonal differences is one in each case. This is consistent with the graphical evidence: the level series should not be modelled as stationary without transformation.

Several additional features in Table 1 add nuance. The Hurst coefficient is very close to one, which is another sign of long memory and strong persistence. Spectral entropy is relatively low, indicating that the series has a structured time-series pattern rather than behaving like white noise. The spikiness measure is very low, suggesting that the whole series is not dominated by isolated erratic spikes, even though there are clearly historically important shocks. The shift-level and shift-variance indicators point to meaningful changes in the level and variability of the series, which is plausible for a sample that includes the late-1990s shock, the global financial crisis and COVID-19. The ARCH-related statistic does not suggest that volatility clustering is the central feature of the series; persistence, trend and seasonality are more important.

Table 1. Features of GDP for Serbia time series

| Feature | Value |

|---|---|

| trend_strength | 0.995 |

| seasonal_strength_year | 0.875 |

| seasonal_peak_year | 0 |

| seasonal_trough_year | 1 |

| spikiness | 0.000 |

| linearity | 2.798 |

| curvature | -0.351 |

| stl_e_acf1 | -0.264 |

| stl_e_acf10 | 0.430 |

| acf1 | 0.925 |

| acf10 | 6.446 |

| diff1_acf1 | -0.325 |

| diff1_acf10 | 1.824 |

| diff2_acf1 | -0.520 |

| diff2_acf10 | 2.294 |

| season_acf1 | 0.876 |

| pacf5 | 1.213 |

| diff1_pacf5 | 0.995 |

| diff2_pacf5 | 1.108 |

| season_pacf | 0.309 |

| zero_run_mean | 0.000 |

| nonzero_squared_cv | 0.004 |

| zero_start_prop | 0.000 |

| zero_end_prop | 0.000 |

| lambda_guerrero | 2.000 |

| kpss_stat | 2.416 |

| kpss_pvalue | 0.010 |

| pp_stat | -1.829 |

| pp_pvalue | 0.100 |

| ndiffs | 1 |

| nsdiffs | 1 |

| bp_stat | 106.936 |

| bp_pvalue | 0.000 |

| lb_stat | 109.523 |

| lb_pvalue | 0.000 |

| var_tiled_var | 0.002 |

| var_tiled_mean | 0.996 |

| shift_level_max | 0.112 |

| shift_level_index | 17 |

| shift_var_max | 0.021 |

| shift_var_index | 19 |

| shift_kl_max | 0.206 |

| shift_kl_index | 14 |

| spectral_entropy | 0.270 |

| n_crossing_points | 21 |

| longest_flat_spot | 6 |

| coef_hurst | 0.999 |

| stat_arch_lm | 0.830 |

The main conclusion from Part 1 is that Serbia’s quarterly GDP is a strongly trending, highly persistent and visibly seasonal series. It contains large historical shocks, but the dominant long-run picture is one of recovery and expansion. These properties explain why seasonal adjustment, log transformation and differencing are necessary before moving to short-term forecasting.

Methodological appendix to Part 1

Graphical exploration is the first stage of time-series analysis. It helps identify trends, seasonal patterns, structural breaks, cyclical movements, changes in volatility and outliers. In this case, Figure 1 immediately shows that Serbia’s GDP has a strong upward trend, visible seasonality and several major shocks. The main risk in reading such graphs is to confuse regular seasonal variation with genuine changes in macroeconomic direction. Another risk is to over-interpret a single observation without considering whether it belongs to a broader pattern.

The log transformation is used because many macroeconomic series become more variable in absolute terms as their level rises. A movement of two index points means something different when GDP is low than when GDP is high. Logs help stabilise this relationship and make changes more interpretable as approximate percentage movements. Differencing is then used to remove persistent trend and seasonal structure. A first difference focuses on quarter-to-quarter change, while a seasonal difference compares a quarter with the same quarter in the previous year.

The time-series features in Table 1 summarise the statistical behaviour of the series. Trend strength measures how dominant the long-run component is. Seasonal strength measures the importance of recurring intra-year patterns. Autocorrelation and partial autocorrelation features show how strongly the series depends on its past. KPSS and related diagnostics help assess stationarity. Entropy, spikiness and shift measures describe whether the series is noisy, irregular or affected by structural changes. These indicators should not be read mechanically, but together they confirm that Serbia’s GDP is a persistent, seasonal and non-stationary macroeconomic series.